Will A Decade of Lower Than Average Returns Impact My FIRE Date?

Most major investment firms are predicting lower than average returns for the stock market in the next decade. Horrifying words like Lost Decade are being thrown around. Even the vaunted Vanguard stock outlook has market returns in the 5.5% to 7.5% nominal annualized range for the next 10 years. This Vanguard report was recently updated over the summer after an even worse December 2019 outlook of 4%-ish returns.

International equity growth seems to fare better when modeled by all parties. Vanguard has International equities returning 8.5%-10.5% nominal annualized returns.

Vanguard’s ’20s Outlook

Here’s a look at who’s saying what.

- Blackstone executive vice-chair Tony James predicts a “lost decade”.

- Research Affiliates 1.5% returns over the next decade.

- Morningstar 4.6% returns 10 year outlook.

- JP Morgan 5.6% returns in 10-15 year outlook and emerging market returns of 8.5%-8.7%. From their 116 page report Long Term Capital Market Assumptions.

- Goldman Sachs 6% stock returns 10 year outlook.

- Deutche Bank 2030 report. Not much for specific stock return forecasting, but a very interesting read from a European paradigm.

- Bank of America is predicting annual returns of 3%-4% over the next decade. They also give an S&P target of 5,200 points…roughly 45% higher than its trading now.

- Schwab 7% return. This is one of the more optimistic outlooks for the 20’s.

- Big ERN predicts 6% Returns. Not a brokerage firm, but I really respect his work. Note this post is from 2017. His formulas breakdown why lower returns are expected (almost needed to right the valuations) next decade.

Schwab’s Forecast

So what’s an index fund investor to do with all these depressing predictions for the next decade? How can anyone expect to FIRE in the near future if returns are below the 8% average return, and if the “experts” are right, returns will be anywhere between 1%-7%—just take a look at that giant range. The range itself should give us a clue to how accurate predictions are.

Things look bad. So what now?

Okay, so now that I’ve gotten all these pessimistic predictions for the next decade out of the way. What will I change about my own investment strategy to meet this outlook? Become a dividend investor and lose out on growth, pay more taxes, and possibly invest in a company that goes bankrupt? Invest way more into real estate? Go all out on international funds?

I will do nothing different than to keep to the plan and maintain the general course. I based my Retire Early year (2026) on a 7% annual return. What had been conservative to me then, is apparently boyishly optimistic now–according to Wall Street analysts.

Type-A worriers raise your hand

Am I worried about this imaginary scenario of a bad decade for stock growth? Sadly, yes. I’m a worrier by nature. And some of these arguments and predictions by a consensus of experts who spend their lives analyzing the market sound pretty convincing to this construction worker. Who am I to argue that they are wrong?

But why does this worry me? Because I want to retire as soon as I can. I want out of this rat race. I want to be there full time while my kids are still young. Low market returns add more years that I have to get to commute and work in the high-stress environment that commercial construction is.

All these “low market return” articles and predictions I’m seeing just add to the fire of anxiety that I’m naturally inclined towards. I’m constantly in a battle with myself imagining unlikely future scenarios, and then endlessly worrying about them. But because I’m a worrier, and have been for some time, I know how to fight the needless worry about things that haven’t or may not ever happen. Part of that strategy is talking about how irrational predicting the future is (hence this post) and focusing on the present moment.

Being present is important

Here is a wonderful excerpt from The Wisdom of Insecurity by Alan Watts. This entire book is filled with outstanding eastern philosophic material, but this paragraph has stuck with me over the years. I think about it a great deal when I worry.

What is the use of planning to be able to eat next week unless I can really enjoy the meals when they come? If I am busy planning how to eat next week that I cannot fully enjoy what I am eating now, I will be in the same predicament when next week’s meals become “now.”

Alan Watts

Being present is important. Meditating helps me break free of worrying about the future. It’s our human nature to want, but want brings suffering: I want higher returns so I can retire sooner; I want to have a happy life with my family; I want something to be different than this moment….

My optimistic reasoning for not getting too worked up about a possible decade of low returns:

(I do acknowledge the fundamentals of why lower returns are expected and highly likely despite my naive optimism. But let me dream.)

#1. These so-called predictions are made by firms with one audience in mind: their clients.

Lowering expectations is a smart and common business strategy. If the bar is lowered, it’s easy to beat expectations and come out looking like you are providing a valuable service to your clients. After the Great Recession, hardly anyone (Vanguard came close) predicted the massive bull run returns that would last till 2020.

For these hedge fund managers, this is how they come out looking shiny if they can slightly outperform their own low bars.

#2. Another reason to read these low return scenarios with skepticism goes back to how these firms are making money.

They want their clients to schedule meetings and begin shifting money around. This is how they make money. Analysts are saying that emerging international markets will soon outpace our domestic powerhouse benchmarks—at least in the near future. They want their clients to start rebalancing…realize those capital gains. Sell those loaded funds. Sell what you’ve made in the last decade…and then buy what we’re offering you.

#3. We can’t predict the future of the stock market (or the future in general).

There’s always going to be doom and gloom writers and economists. This type of writing sells. The saying that we “shouldn’t worry about what we cannot control” applies nicely here.

As investors looking for average returns, we can only control where we put our money and associated fees. Trying to predict the market is like scientists trying to predict earthquakes…you just can’t. They can only look back and analyze past trends and data and then compare this data to the information we have at the present moment. Like I’m going to do below…

#4. There can be two decades of above-average growth in a row. Look at the ’80s and ’90s.

The historic trend of the stock market is that stocks underperform after periods of above-average growth. If you look at the Annual Returns column you will see the pattern. Then we get to the ’80s and ’90s.

Why can’t the 2010s and 2020s be another double decade of great growth?

Even if there’s a decade of low returns, you can still make money in the market

So how do you make money in a Lost Decade? It starts with continually putting money in the market. I will have to simply keep doing what I’m doing. Invest on a weekly basis and keep my savings rate at or above 50%.

Will lower stock market returns mean that I’ll stop getting raises or bonuses at work? Likely not. Not unless there’s a full-blown recession or depression–which in that case I may be out of work altogether. Any raises I do get will be added to investments. Bonuses? Straight to the market.

And if things get worse, like Lost Decade worse, we will cost average our way down with the bear market. This is an interesting NYT article from 2010, arguing why Lost Decades aren’t really lost.

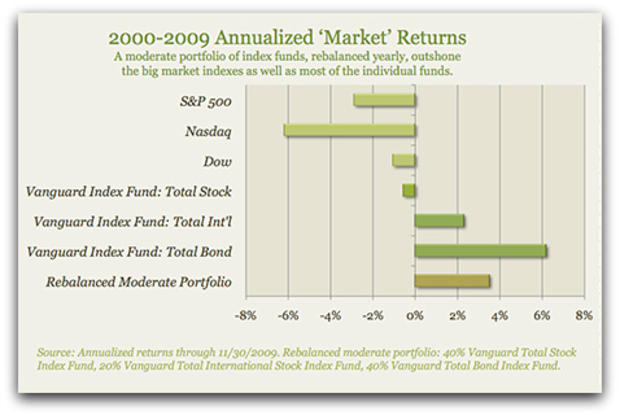

Look at the below graphic. See how the Vanguard big boy funds fared during the lost decade? Not too shabby for a Lost Decade. Now imagine you are constantly buying shares on the way up…your returns would be better than this.

You only don’t make money in a Lost Decade if you are letting your investments sit and do not cost average in new capital and reinvest your dividends.

Is Retiring Early possible in a Lost Decade?

Of course it is. And we will FIRE by the mid 20s one way or another. The key will be maintaining the course and being able to adapt. The 3 factors for our FIRE Triangle will remain the same.

The biggest problem posed would be, taking a little longer to hit our FI number. A year or two or three “might” be added on to our timeline, so therefore I’d retire at 44 instead of 42…not the end of the world. Or we could pull the trigger in 2026 regardless and just move to Vietnam.

But alas, I’m again worrying about things that have yet to occur, and may very well never occur.

Discover more from Happily Disengaged

Subscribe to get the latest posts sent to your email.

17 thoughts on “Will A Decade of Lower Than Average Returns Impact My FIRE Date?”

Raising a hand! Type A worrier here! Still, we don’t plan on changing much. Once we get these rental properties paid off we’ll increase our investment portfolio but for fight now, staying the course. We’re with you. We want out of this rat race to. We HATE IT!!

Retiring at 44 is still better (much better) than retiring are never.

Great read. Thanks!

Right on. Staying the course and ignoring the noise is the surest way to FI. Thanks the comment

Good article thanks for sharing. As you brought up that saying that we “shouldn’t worry about what we cannot control” applies here. However, what we can control is the fire to achieve FIRE. Pun intendended 🙂 – best of luck in your journey!

That’s right, we control our motivation and drive. Appreciate your comment

Certainly feels like we’re due for a bit slower growth, but I probably would have said the same thing four years ago. I think it’s more important that you’re aware of lower returns being a possible outcome, but not to let it impact your strategy. Hopefully the next decade exceeds expectations!

Agreed. I’m staying the course, my expectations have been lowered a bit from all the pessimism, but that’s not a bad thing. Better to be surprised by higher returns than lower ones. Thanks for commenting.

Noel,

Thanks for sharing this meta-analysis! I think it’s a good reminder for why a lot of FIRE proponents (I’m looking at you Bogleheads) support the idea of a diversified portfolio. For example, VTSAX and nothing else isn’t necessarily all that diversified. Perhaps a “three-fund portfolio” helps avoid that.

Yea I agree Chris. A little international might help buoy the returns over the next few years and make for a smoother ride.

Here from europe we always feel, there is too much US Stocks in Our Portfolio 😉

Many do a market value equivalent, which is roughly 70 % Msci World plus 30 % Msci Emerging Markets (Vanguard still not so big over here).

This gives me a Portfolio with about 50 % US, which still feels a lot to me.

Haha, forgot my conclusion.

What I tried to say. My net Worth is 50 % in a country I never saw. So you should try stop shying away from other Markets, at least a little.

Those other markets are bound to rally at some point. Don’t miss out on this opportunity.

Haha, forgot my conclusion.

What I tried to say. My net Worth is 50 % in a country I never saw. So you should try stop shying away from other Markets, at least a little.

Those other markets are bound to rally at some point. Don’t miss out on this opportunity.

Hey Silke- I appreciate your perspective from Europe. I think it’s very valuable. You make a good point that eventually international will catch up. There’s definitely a bias over here because of the recent American market returns and because, well people in America are “cautious” about things not American. I try not to let that influence me.

I’m getting there though, I truly believe one day American markets will mellow and international will start ramping up returns as super powers change. Look at China! I’m slowly allocating more to international. Right now I’m at 20%. I plan on living overseas in early retirement, so more international wouldn’t hurt to balance things. Thanks for reading and commenting!!

Hey, i had more time to think about it.

What we want is about growth and when I was in China I saw a lot of poor people working hard, often sucessfully, for a life we still consider as poor. Let’s say to buy a first fridge in the family. And when I read UN reports, I learn there are millions, tens of or hundreds out in the world who are doing this step. So the big growth potential in markets is maybe not buy a bigger car in europe or the US, but buy a fridge, a washing maschine, furniture and three pair of shoes per person, buy electricity and tap water and internet from your town somewhere in Asia, South American or Africa. A completely different potential than we experience in our daily life. Great for them people – a big chance for us, if we are invested in these markets.

Oh yea I agree. I actually bought some foreign individual stock last week thinking about this too. BABA and JD. Their Singles Day sales revenue was something like $115 billion. Crazy